"""Jupytext source for the CDS-bond basis project tour notebook."""

'Jupytext source for the CDS-bond basis project tour notebook.'

CDS-Bond Basis Replication: Project Tour#

This notebook is the high-level walkthrough of our CDS-bond basis replication workflow. It documents what we replicate, which data we use, the main pipeline steps, and the final outputs used in the report/site.

1. Replication Goal#

We focus on the CDS-bond basis component from Siriwardane, Sunderam, and Wallen’s Segmented Arbitrage:

Bond-level basis:

cds_basis_spread = par_spread - z_spreadIn basis points:

cds_basis_spread_bps = cds_basis_spread * 10000

The objective is to produce clean bond-level and aggregated time series (Investment Grade vs High Yield), plus diagnostics and summary statistics.

2. Data Sources (Current Pipeline)#

WRDS Markit CDS (

markit_cds.parquet)redcode,date,tenor,parspread

WRDS RED mapping (

RED_and_ISIN_mapping.parquet)maps ISIN to RED entity code

WRDS bond returns (

wrds_bondret_project.parquet)bond characteristics and pricing inputs

CRSP Treasury + Fed yield curve

curve fitting for z-spread, with Fed fallback checks on problematic dates

Current final analysis files:

_data/cds_basis_processed.parquet_data/cds_basis_aggregated.parquet_data/cds_basis_non_aggregated.parquet_data/cds_basis_summary_stats.csv

3. Pipeline Steps Implemented#

Pull and clean bond/CDS/mapping datasets.

Merge bonds to CDS entities via ISIN->REDCODE mapping.

Interpolate CDS par spreads at bond maturity horizon.

Estimate bond z-spreads from pricing equations.

Compute CDS-bond basis spread and aggregate by rating/date.

Export datasets, chart, and summary stats.

from pathlib import Path

import matplotlib.pyplot as plt

import pandas as pd

import seaborn as sns

import chartbook

BASE_DIR = chartbook.env.get_project_root()

DATA_DIR = BASE_DIR / "_data"

4. Load Final Processed Data#

agg_df = pd.read_parquet(DATA_DIR / "cds_basis_aggregated.parquet")

non_agg_df = pd.read_parquet(DATA_DIR / "cds_basis_non_aggregated.parquet")

stats_df = pd.read_csv(DATA_DIR / "cds_basis_summary_stats.csv")

print("=== Aggregated Dataset ===")

print(f"Shape: {agg_df.shape}")

print(f"Date range: {agg_df['date'].min()} to {agg_df['date'].max()}")

print(f"Rating buckets: {agg_df['c_rating'].unique().tolist()}")

if "analysis_period" in agg_df.columns:

print(f"Analysis periods: {agg_df['analysis_period'].dropna().unique().tolist()}")

print("\n=== Non-Aggregated Dataset ===")

print(f"Shape: {non_agg_df.shape}")

print(f"Date range: {non_agg_df['date'].min()} to {non_agg_df['date'].max()}")

id_col = "isin" if "isin" in non_agg_df.columns else "cusip"

print(f"Unique IDs ({id_col}): {non_agg_df[id_col].nunique()}")

=== Aggregated Dataset ===

Shape: (604, 10)

Date range: 2010-01-31 00:00:00 to 2024-12-31 00:00:00

Rating buckets: ['High Yield', 'Investment Grade']

Analysis periods: ['replication_2010_2020', 'full_period_2010_2024']

=== Non-Aggregated Dataset ===

Shape: (204899, 10)

Date range: 2010-01-31 00:00:00 to 2024-12-31 00:00:00

Unique IDs (isin): 2243

5. Summary Statistics#

print("Project summary stats table:")

display(stats_df)

if "analysis_period" in agg_df.columns:

for period in sorted(agg_df["analysis_period"].dropna().unique()):

agg_wide = agg_df[agg_df["analysis_period"] == period].pivot(

index="date", columns="c_rating", values="cds_basis_spread_bps"

)

print(f"\nAggregated CDS-bond basis spread (bps) by rating [{period}]:")

display(agg_wide.describe().T)

else:

agg_wide = agg_df.pivot(index="date", columns="c_rating", values="cds_basis_spread_bps")

print("\nAggregated CDS-bond basis spread (bps) by rating:")

display(agg_wide.describe().T)

print("\nBond-level CDS-bond basis spread stats (bps):")

display(non_agg_df["cds_basis_spread_bps"].describe())

Project summary stats table:

| group | n_obs | start_date | end_date | mean_bps | median_bps | std_bps | analysis_period | period_label | period_start | period_end | |

|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | All bonds | 122 | 2010-01-31 | 2020-02-29 | -55.102355 | -56.172446 | 21.139116 | replication_2010_2020 | Replication (2010-01-01 to 2020-02-29) | 2010-01-01 | 2020-02-29 |

| 1 | Investment Grade | 122 | 2010-01-31 | 2020-02-29 | -43.852373 | -42.835425 | 18.198621 | replication_2010_2020 | Replication (2010-01-01 to 2020-02-29) | 2010-01-01 | 2020-02-29 |

| 2 | High Yield | 122 | 2010-01-31 | 2020-02-29 | -88.019349 | -84.569900 | 35.462100 | replication_2010_2020 | Replication (2010-01-01 to 2020-02-29) | 2010-01-01 | 2020-02-29 |

| 3 | All bonds | 180 | 2010-01-31 | 2024-12-31 | -48.714874 | -43.748939 | 28.092973 | full_period_2010_2024 | Full Period (2010-01-01 to 2024-12-31) | 2010-01-01 | 2024-12-31 |

| 4 | Investment Grade | 180 | 2010-01-31 | 2024-12-31 | -38.772864 | -33.678487 | 23.191339 | full_period_2010_2024 | Full Period (2010-01-01 to 2024-12-31) | 2010-01-01 | 2024-12-31 |

| 5 | High Yield | 180 | 2010-01-31 | 2024-12-31 | -76.822096 | -78.750047 | 50.625029 | full_period_2010_2024 | Full Period (2010-01-01 to 2024-12-31) | 2010-01-01 | 2024-12-31 |

Aggregated CDS-bond basis spread (bps) by rating [full_period_2010_2024]:

| count | mean | std | min | 25% | 50% | 75% | max | |

|---|---|---|---|---|---|---|---|---|

| c_rating | ||||||||

| High Yield | 180.0 | -76.822096 | 50.625029 | -271.396379 | -106.099087 | -78.750047 | -42.996925 | 62.555892 |

| Investment Grade | 180.0 | -38.772864 | 23.191339 | -188.552595 | -51.731793 | -33.678487 | -22.808611 | -6.104417 |

Aggregated CDS-bond basis spread (bps) by rating [replication_2010_2020]:

| count | mean | std | min | 25% | 50% | 75% | max | |

|---|---|---|---|---|---|---|---|---|

| c_rating | ||||||||

| High Yield | 122.0 | -88.019349 | 35.462100 | -197.885137 | -113.457249 | -84.569900 | -61.745672 | -19.913129 |

| Investment Grade | 122.0 | -43.852373 | 18.198621 | -88.114059 | -56.272803 | -42.835425 | -27.605197 | -12.370801 |

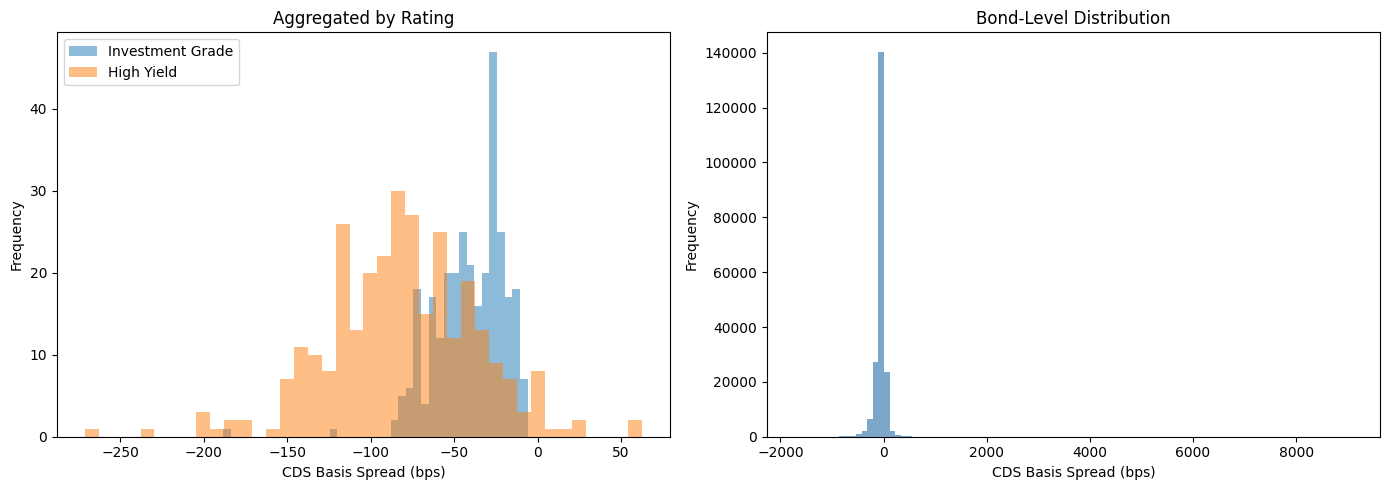

Bond-level CDS-bond basis spread stats (bps):

count 204899.000000

mean -53.192067

std 107.441160

min -1722.708802

25% -81.288627

50% -39.921375

75% -11.960890

max 9084.999656

Name: cds_basis_spread_bps, dtype: float64

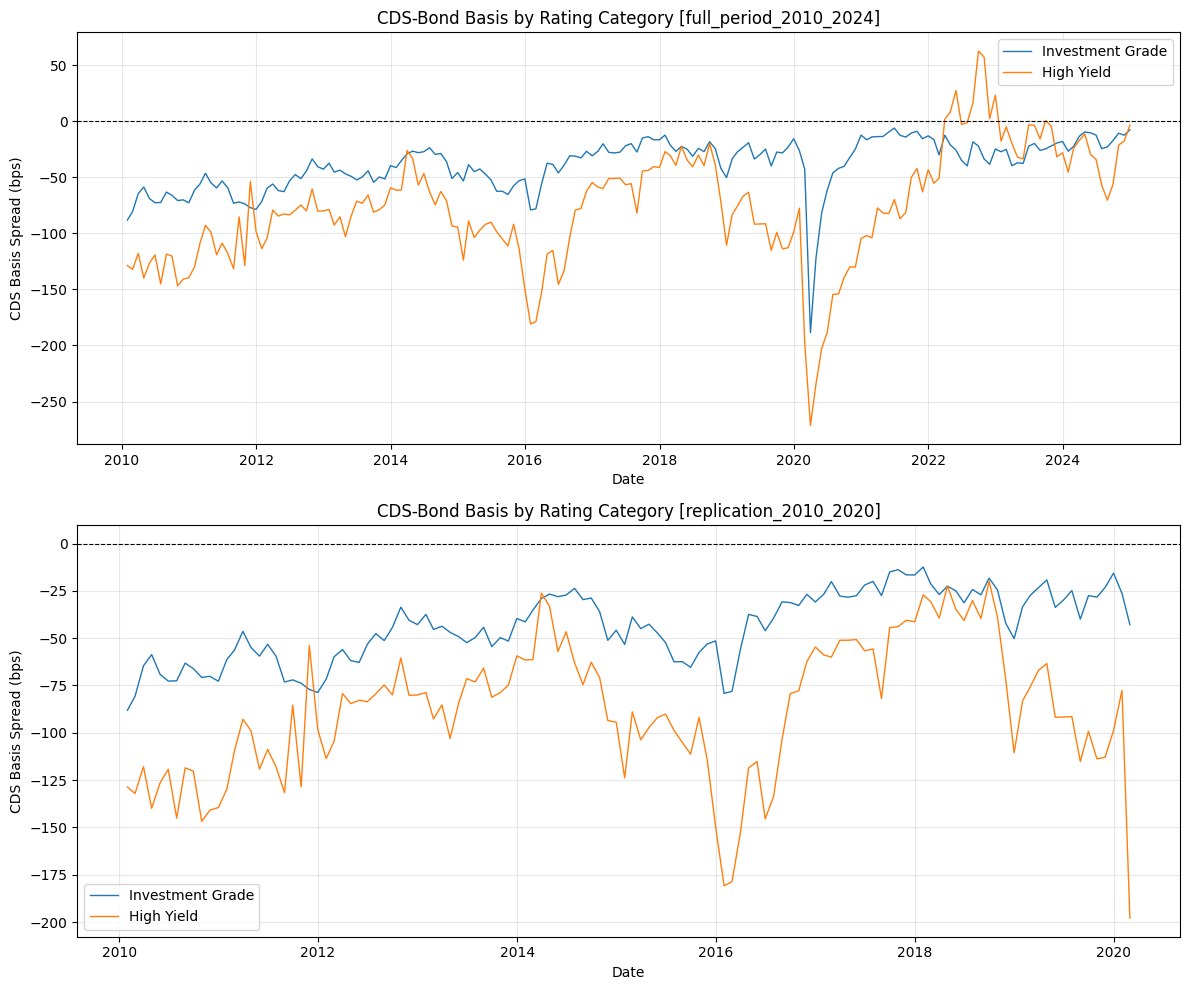

6. Time Series: Basis by Rating#

if "analysis_period" in agg_df.columns:

periods = sorted(agg_df["analysis_period"].dropna().unique())

fig, axes = plt.subplots(len(periods), 1, figsize=(12, 5 * len(periods)), sharex=False)

if len(periods) == 1:

axes = [axes]

for ax, period in zip(axes, periods):

g = agg_df[agg_df["analysis_period"] == period]

for rating in ["Investment Grade", "High Yield"]:

s = g[g["c_rating"] == rating].sort_values("date")

ax.plot(s["date"], s["cds_basis_spread_bps"], label=rating, linewidth=1.0)

ax.axhline(0, color="black", linewidth=0.8, linestyle="--")

ax.set_xlabel("Date")

ax.set_ylabel("CDS Basis Spread (bps)")

ax.set_title(f"CDS-Bond Basis by Rating Category [{period}]")

ax.legend(loc="best")

ax.grid(True, alpha=0.3)

plt.tight_layout()

plt.show()

else:

fig, ax = plt.subplots(figsize=(12, 6))

for rating in ["Investment Grade", "High Yield"]:

s = agg_df[agg_df["c_rating"] == rating].sort_values("date")

ax.plot(s["date"], s["cds_basis_spread_bps"], label=rating, linewidth=1.0)

ax.axhline(0, color="black", linewidth=0.8, linestyle="--")

ax.set_xlabel("Date")

ax.set_ylabel("CDS Basis Spread (bps)")

ax.set_title("CDS-Bond Basis by Rating Category")

ax.legend(loc="best")

ax.grid(True, alpha=0.3)

plt.tight_layout()

plt.show()

7. Distribution Checks#

fig, axes = plt.subplots(1, 2, figsize=(14, 5))

for rating in ["Investment Grade", "High Yield"]:

subset = agg_df[agg_df["c_rating"] == rating]

axes[0].hist(subset["cds_basis_spread_bps"], bins=40, alpha=0.5, label=rating)

axes[0].set_xlabel("CDS Basis Spread (bps)")

axes[0].set_ylabel("Frequency")

axes[0].set_title("Aggregated by Rating")

axes[0].legend()

axes[1].hist(non_agg_df["cds_basis_spread_bps"], bins=100, alpha=0.7, color="steelblue")

axes[1].set_xlabel("CDS Basis Spread (bps)")

axes[1].set_ylabel("Frequency")

axes[1].set_title("Bond-Level Distribution")

plt.tight_layout()

plt.show()

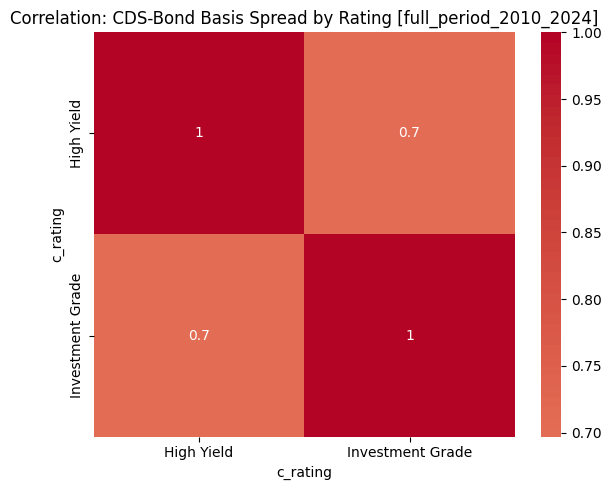

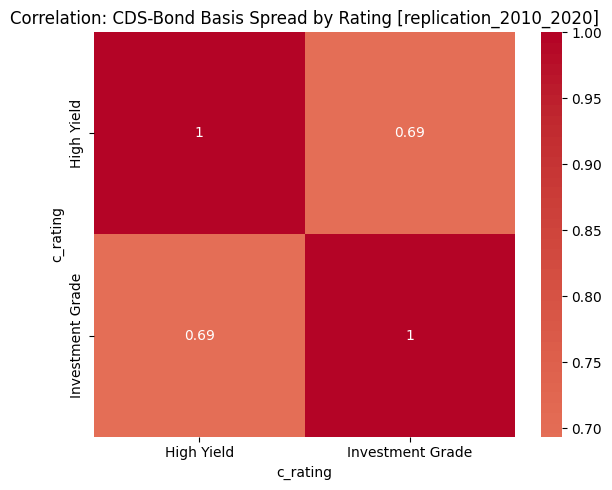

8. Correlation Across Rating Buckets#

if "analysis_period" in agg_df.columns:

for period in sorted(agg_df["analysis_period"].dropna().unique()):

agg_wide = agg_df[agg_df["analysis_period"] == period].pivot(

index="date", columns="c_rating", values="cds_basis_spread_bps"

)

if len(agg_wide.columns) > 1:

corr_matrix = agg_wide.corr()

print(f"Correlation matrix [{period}]:")

display(corr_matrix)

fig, ax = plt.subplots(figsize=(6, 5))

sns.heatmap(corr_matrix, annot=True, cmap="coolwarm", center=0, ax=ax)

ax.set_title(f"Correlation: CDS-Bond Basis Spread by Rating [{period}]")

plt.tight_layout()

plt.show()

else:

if len(agg_wide.columns) > 1:

corr_matrix = agg_wide.corr()

print("Correlation matrix:")

display(corr_matrix)

fig, ax = plt.subplots(figsize=(6, 5))

sns.heatmap(corr_matrix, annot=True, cmap="coolwarm", center=0, ax=ax)

ax.set_title("Correlation: CDS-Bond Basis Spread by Rating")

plt.tight_layout()

plt.show()

Correlation matrix [full_period_2010_2024]:

| c_rating | High Yield | Investment Grade |

|---|---|---|

| c_rating | ||

| High Yield | 1.00000 | 0.69696 |

| Investment Grade | 0.69696 | 1.00000 |

Correlation matrix [replication_2010_2020]:

| c_rating | High Yield | Investment Grade |

|---|---|---|

| c_rating | ||

| High Yield | 1.000000 | 0.693878 |

| Investment Grade | 0.693878 | 1.000000 |

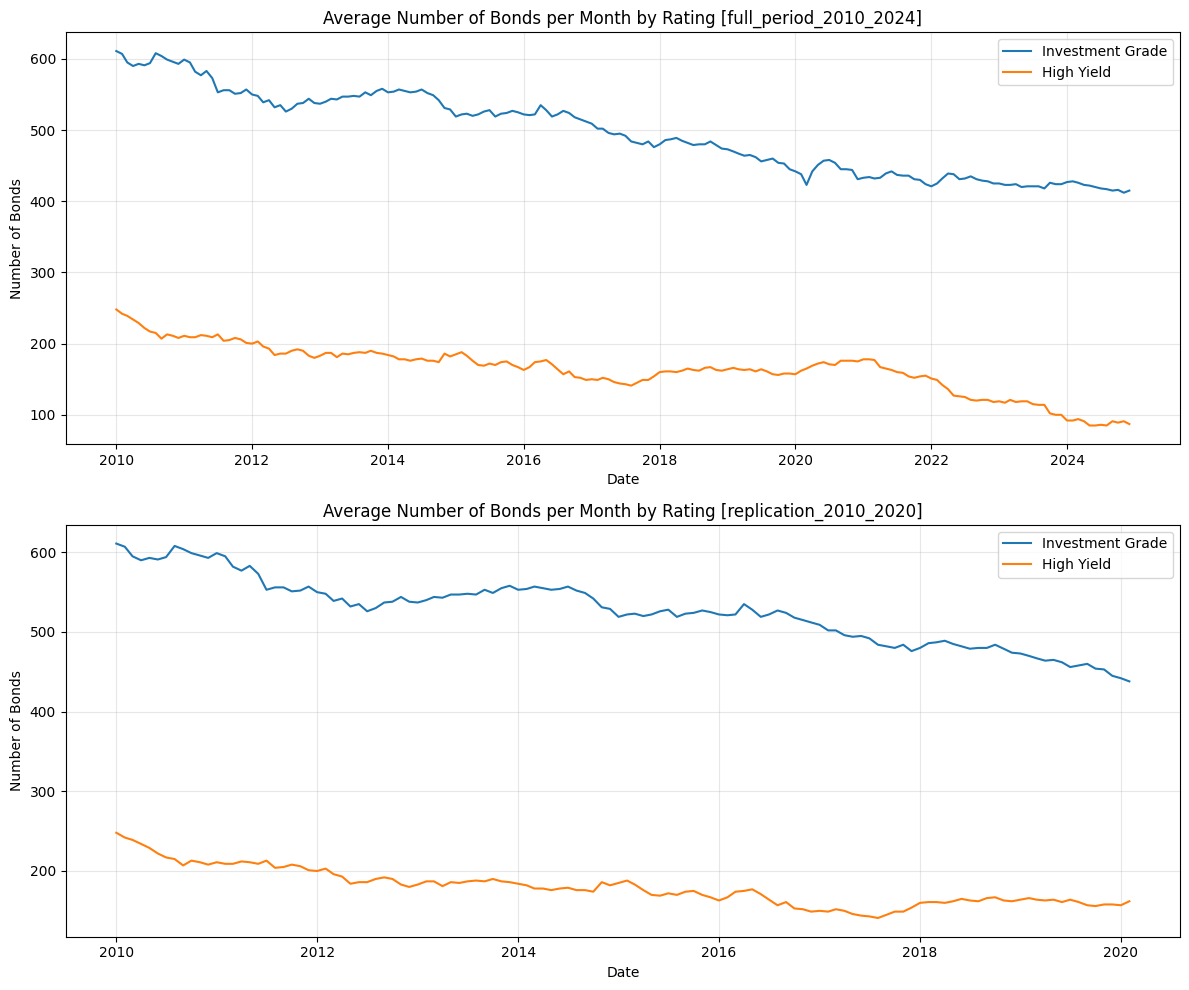

9. Monthly Counts and Data Quality#

agg_df["date"] = pd.to_datetime(agg_df["date"])

if "analysis_period" in agg_df.columns:

periods = sorted(agg_df["analysis_period"].dropna().unique())

fig, axes = plt.subplots(len(periods), 1, figsize=(12, 5 * len(periods)), sharex=False)

if len(periods) == 1:

axes = [axes]

for ax, period in zip(axes, periods):

g = agg_df[agg_df["analysis_period"] == period]

monthly_counts = (

g.groupby([g["date"].dt.to_period("M"), "c_rating"])["n_bonds"]

.mean()

.reset_index()

)

monthly_counts["date"] = monthly_counts["date"].dt.to_timestamp()

for rating in ["Investment Grade", "High Yield"]:

s = monthly_counts[monthly_counts["c_rating"] == rating]

ax.plot(s["date"], s["n_bonds"], label=rating)

ax.set_title(f"Average Number of Bonds per Month by Rating [{period}]")

ax.set_xlabel("Date")

ax.set_ylabel("Number of Bonds")

ax.grid(alpha=0.3)

ax.legend()

plt.tight_layout()

plt.show()

else:

monthly_counts = (

agg_df.groupby([agg_df["date"].dt.to_period("M"), "c_rating"])["n_bonds"]

.mean()

.reset_index()

)

monthly_counts["date"] = monthly_counts["date"].dt.to_timestamp()

fig, ax = plt.subplots(figsize=(12, 5))

for rating in ["Investment Grade", "High Yield"]:

s = monthly_counts[monthly_counts["c_rating"] == rating]

ax.plot(s["date"], s["n_bonds"], label=rating)

ax.set_title("Average Number of Bonds per Month by Rating")

ax.set_xlabel("Date")

ax.set_ylabel("Number of Bonds")

ax.grid(alpha=0.3)

ax.legend()

plt.tight_layout()

plt.show()

print("Missing values (aggregated bps):", agg_df["cds_basis_spread_bps"].isna().sum())

print("Missing values (non-aggregated bps):", non_agg_df["cds_basis_spread_bps"].isna().sum())

Missing values (aggregated bps): 0

Missing values (non-aggregated bps): 0

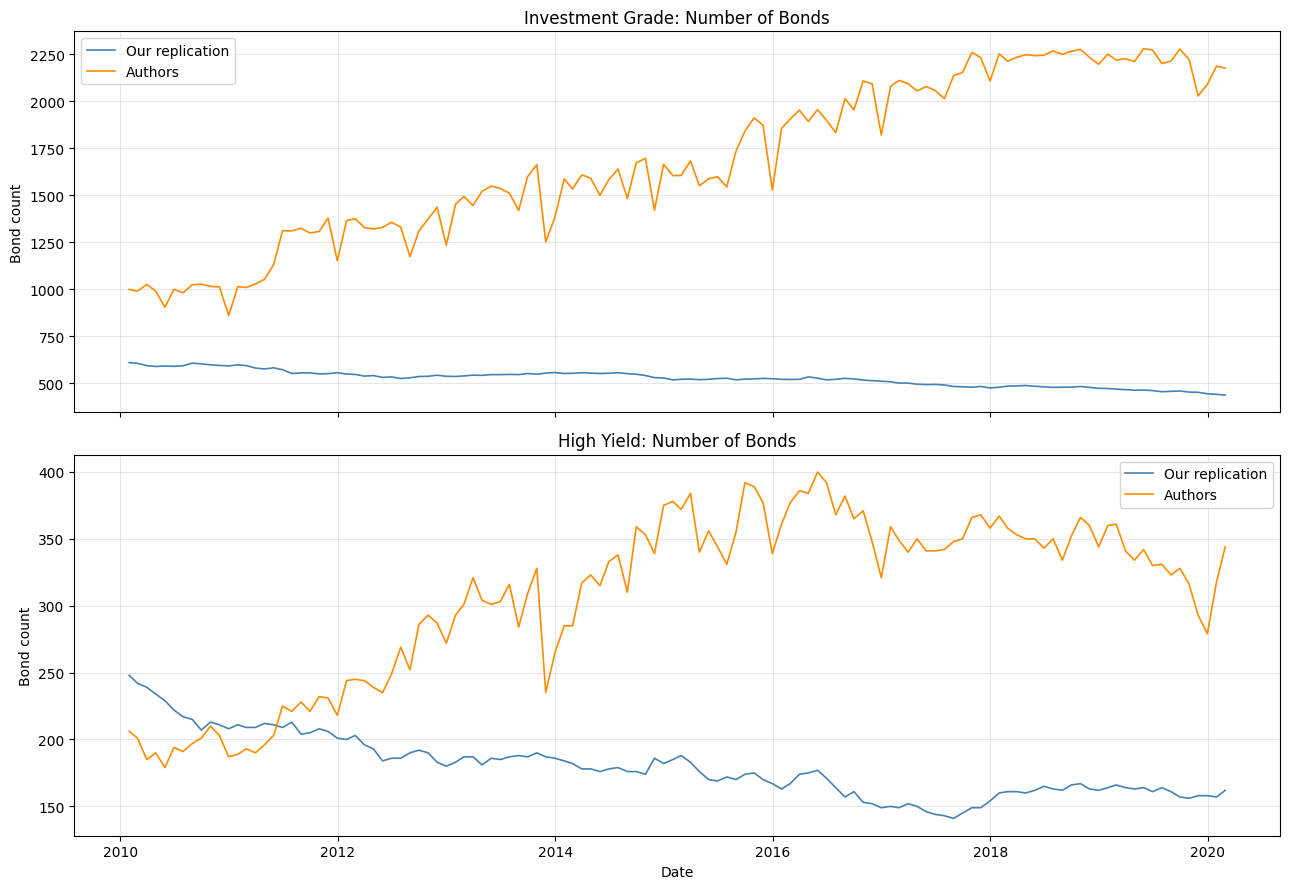

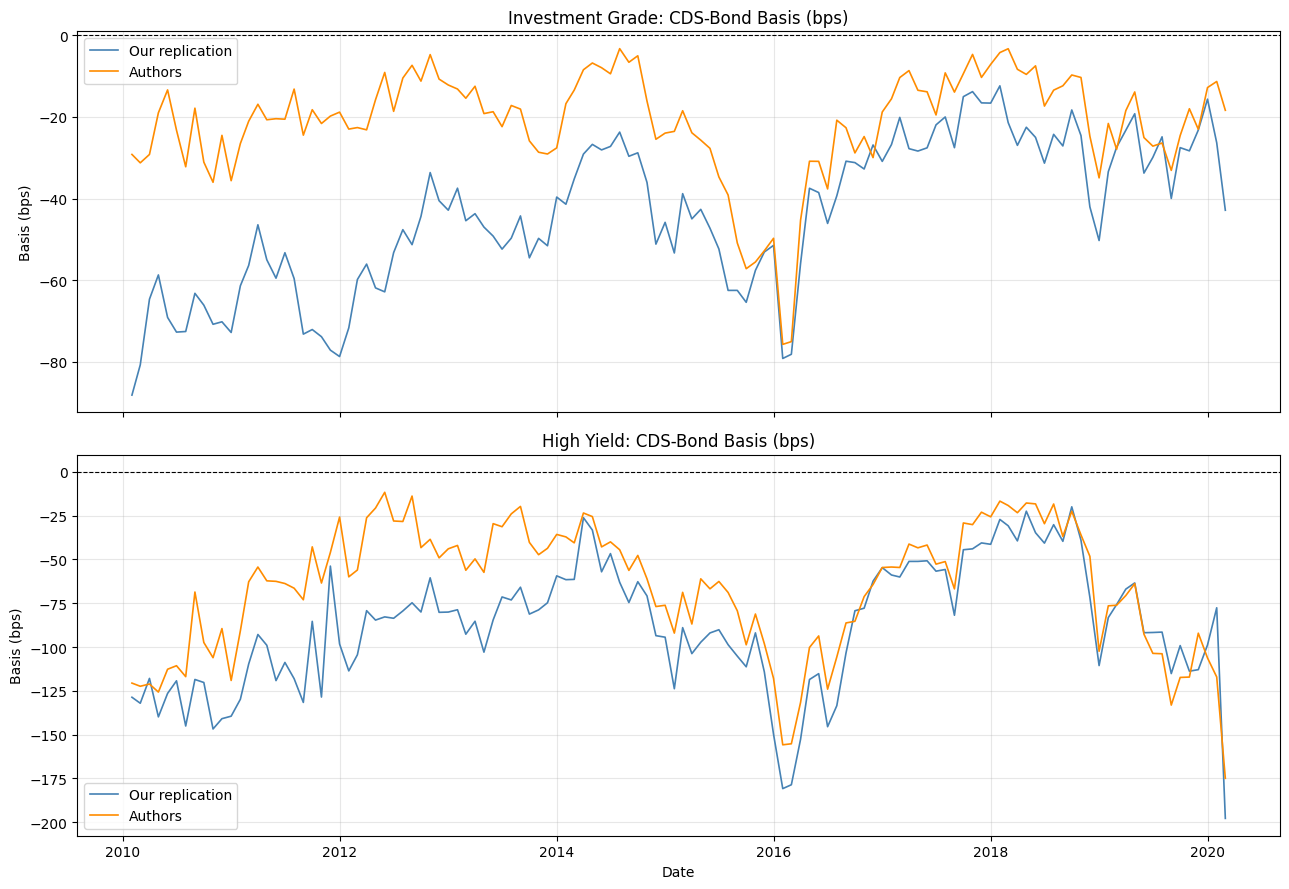

10. Comparison with Authors (Replication Window)#

This section compares our replication to the authors’ dataset over the replication window (2010-01-01 to 2020-02-29).

Basis spread comparison in bps (monthly)

Bond-count comparison (monthly)

Side-by-side summary table (mean/median/std + bond-count moments)

authors_path = BASE_DIR / "data_manual" / "cds_paper_data.xlsx"

sheet_candidates = ["basis", "Bases"]

xl = pd.ExcelFile(authors_path)

sheet_name = next((s for s in sheet_candidates if s in xl.sheet_names), None)

if sheet_name is None:

raise ValueError(

f"Could not find any of {sheet_candidates} in {authors_path}. "

f"Found sheets: {xl.sheet_names}"

)

authors_df = pd.read_excel(authors_path, sheet_name=sheet_name).copy()

authors_df.columns = [c.strip() for c in authors_df.columns]

colmap = {c.lower(): c for c in authors_df.columns}

date_col = colmap.get("date")

basis_col = colmap.get("cds_bond_basis")

rating_col = colmap.get("ratingbin")

bond_count_col = colmap.get("bond_count")

if not all([date_col, basis_col, rating_col, bond_count_col]):

raise ValueError(f"Unexpected authors columns: {authors_df.columns.tolist()}")

# Parse messy date values robustly.

raw_date = authors_df[date_col]

parsed_date = pd.to_datetime(raw_date, errors="coerce")

needs_serial = raw_date.notna() & parsed_date.isna()

if needs_serial.any():

serial = pd.to_numeric(raw_date[needs_serial], errors="coerce")

parsed_date.loc[needs_serial] = pd.to_datetime(

serial, unit="D", origin="1899-12-30", errors="coerce"

)

authors_df["date"] = parsed_date

authors_df["cds_bond_basis"] = pd.to_numeric(authors_df[basis_col], errors="coerce")

authors_df["bond_count"] = pd.to_numeric(authors_df[bond_count_col], errors="coerce")

authors_df["c_rating"] = (

authors_df[rating_col].astype(str).str.strip().str.upper().map(

{"IG": "Investment Grade", "HY": "High Yield"}

)

)

authors_df = authors_df.dropna(subset=["date", "cds_bond_basis", "bond_count", "c_rating"]).copy()

rep_start = pd.Timestamp("2010-01-01")

rep_end = pd.Timestamp("2020-02-29")

authors_df = authors_df[(authors_df["date"] >= rep_start) & (authors_df["date"] <= rep_end)].copy()

authors_monthly = (

authors_df.sort_values("date")

.assign(month=lambda d: d["date"].dt.to_period("M"))

.groupby(["month", "c_rating"], as_index=False)

.tail(1)

.copy()

)

authors_monthly["date"] = authors_monthly["month"].dt.to_timestamp("M")

authors_monthly["cds_basis_spread_bps"] = authors_monthly["cds_bond_basis"] * 10000.0

authors_monthly["n_bonds"] = pd.to_numeric(authors_monthly["bond_count"], errors="coerce")

authors_monthly = authors_monthly[["date", "c_rating", "cds_basis_spread_bps", "n_bonds"]]

authors_monthly = authors_monthly.sort_values(["date", "c_rating"]).reset_index(drop=True)

our_rep = agg_df.copy()

if "analysis_period" in our_rep.columns:

our_rep = our_rep[our_rep["analysis_period"] == "replication_2010_2020"].copy()

else:

our_rep = our_rep[(our_rep["date"] >= rep_start) & (our_rep["date"] <= rep_end)].copy()

our_rep["date"] = pd.to_datetime(our_rep["date"], errors="coerce")

our_rep = our_rep.dropna(subset=["date"]).copy()

our_rep = our_rep.sort_values(["date", "c_rating"])

print(f"Authors sheet used: {sheet_name}")

print(

"Our replication monthly rows:", len(our_rep),

"| Authors month-end rows:", len(authors_monthly)

)

Authors sheet used: Bases

Our replication monthly rows: 244 | Authors month-end rows: 244

def _stats_table_for_dataset(df, dataset_name):

rows = []

for rating in ["Investment Grade", "High Yield"]:

sub = df[df["c_rating"] == rating].copy()

rows.append(

{

"dataset": dataset_name,

"rating": rating,

"n_months": int(len(sub)),

"start_date": sub["date"].min() if len(sub) else pd.NaT,

"end_date": sub["date"].max() if len(sub) else pd.NaT,

"mean_bps": float(sub["cds_basis_spread_bps"].mean()) if len(sub) else pd.NA,

"median_bps": float(sub["cds_basis_spread_bps"].median()) if len(sub) else pd.NA,

"std_bps": float(sub["cds_basis_spread_bps"].std()) if len(sub) else pd.NA,

"mean_n_bonds": float(sub["n_bonds"].mean()) if len(sub) else pd.NA,

"median_n_bonds": float(sub["n_bonds"].median()) if len(sub) else pd.NA,

}

)

return pd.DataFrame(rows)

comparison_stats = pd.concat(

[

_stats_table_for_dataset(our_rep, "Our replication"),

_stats_table_for_dataset(authors_monthly, "Authors"),

],

ignore_index=True,

)

print("Replication-window comparison stats (monthly):")

display(comparison_stats)

Replication-window comparison stats (monthly):

| dataset | rating | n_months | start_date | end_date | mean_bps | median_bps | std_bps | mean_n_bonds | median_n_bonds | |

|---|---|---|---|---|---|---|---|---|---|---|

| 0 | Our replication | Investment Grade | 122 | 2010-01-31 | 2020-02-29 | -43.852373 | -42.835425 | 18.198621 | 526.713115 | 528.0 |

| 1 | Our replication | High Yield | 122 | 2010-01-31 | 2020-02-29 | -88.019349 | -84.569900 | 35.462100 | 179.426230 | 176.0 |

| 2 | Authors | Investment Grade | 122 | 2010-01-31 | 2020-02-29 | -21.451358 | -19.073266 | 13.029760 | 1683.934426 | 1607.5 |

| 3 | Authors | High Yield | 122 | 2010-01-31 | 2020-02-29 | -65.978740 | -61.050809 | 35.658357 | 306.139344 | 329.0 |

10.1 Basis Spread (Monthly, bps): Our Replication vs Authors#

fig, axes = plt.subplots(2, 1, figsize=(13, 9), sharex=True)

for ax, rating in zip(axes, ["Investment Grade", "High Yield"]):

s_our = our_rep[our_rep["c_rating"] == rating].sort_values("date")

s_auth = authors_monthly[authors_monthly["c_rating"] == rating].sort_values("date")

ax.plot(

s_our["date"],

s_our["cds_basis_spread_bps"],

label="Our replication",

linewidth=1.2,

color="steelblue",

)

ax.plot(

s_auth["date"],

s_auth["cds_basis_spread_bps"],

label="Authors",

linewidth=1.2,

color="darkorange",

)

ax.axhline(0, color="black", linewidth=0.8, linestyle="--")

ax.set_title(f"{rating}: CDS-Bond Basis (bps)")

ax.set_ylabel("Basis (bps)")

ax.grid(alpha=0.3)

ax.legend(loc="best")

axes[-1].set_xlabel("Date")

plt.tight_layout()

plt.show()

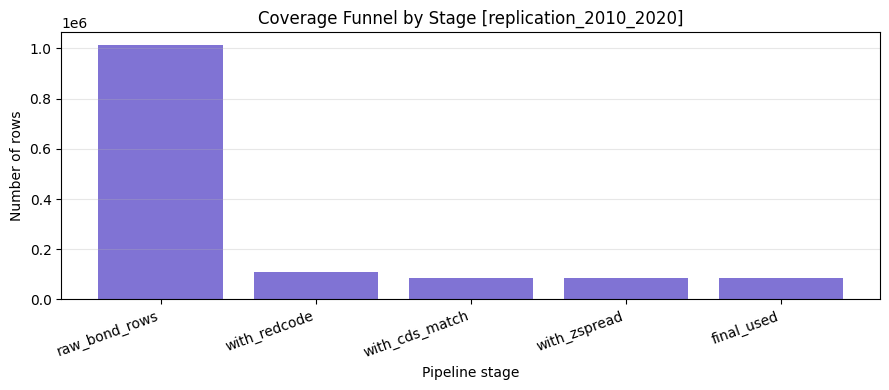

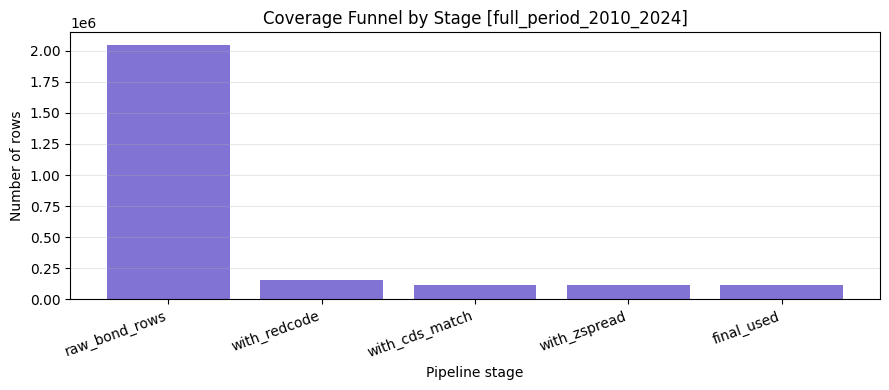

Appendix A. Coverage Funnel Through the Pipeline#

This appendix reports how many observations survive each major step:

Raw bond panel

After RED mapping

After CDS merge/interpolation

With non-missing z-spread

Final processed sample used for basis outputs

raw_bond_df = pd.read_parquet(DATA_DIR / "wrds_bondret_project.parquet")

red_df = pd.read_parquet(DATA_DIR / "red_data.parquet")

final_df = pd.read_parquet(DATA_DIR / "final_data.parquet")

z_df = pd.read_parquet(DATA_DIR / "final_data_with_z_spread.parquet")

processed_df = pd.read_parquet(DATA_DIR / "cds_basis_processed.parquet")

def _id_col(df):

for c in ["isin", "cusip", "i_id"]:

if c in df.columns:

return c

return None

def _filter_period(df, start_date, end_date):

out = df.copy()

if "date" not in out.columns:

return out

out["date"] = pd.to_datetime(out["date"], errors="coerce")

return out[(out["date"] >= start_date) & (out["date"] <= end_date)].copy()

def _count_stage(df, stage_name):

idc = _id_col(df)

return {

"stage": stage_name,

"n_rows": int(len(df)),

"n_unique_ids": int(df[idc].nunique()) if idc is not None else pd.NA,

}

if {"analysis_period", "period_label", "period_start", "period_end"}.issubset(stats_df.columns):

period_meta = (

stats_df[["analysis_period", "period_label", "period_start", "period_end"]]

.drop_duplicates()

.sort_values("period_start")

.copy()

)

else:

period_meta = pd.DataFrame(

[

{

"analysis_period": "replication_2010_2020",

"period_label": "Replication (2010-01-01 to 2020-02-29)",

"period_start": "2010-01-01",

"period_end": "2020-02-29",

},

{

"analysis_period": "full_period_2010_2024",

"period_label": "Full Period (2010-01-01 to 2024-12-31)",

"period_start": "2010-01-01",

"period_end": "2024-12-31",

},

]

)

for _, meta in period_meta.iterrows():

p_name = meta["analysis_period"]

p_label = meta["period_label"]

p_start = pd.Timestamp(meta["period_start"])

p_end = pd.Timestamp(meta["period_end"])

raw_p = _filter_period(raw_bond_df, p_start, p_end)

red_p = _filter_period(red_df, p_start, p_end)

final_p = _filter_period(final_df, p_start, p_end)

z_p = _filter_period(z_df, p_start, p_end)

if "z_spread" in z_p.columns:

z_p = z_p[z_p["z_spread"].notna()].copy()

processed_p = _filter_period(processed_df, p_start, p_end)

funnel = pd.DataFrame(

[

_count_stage(raw_p, "raw_bond_rows"),

_count_stage(red_p, "with_redcode"),

_count_stage(final_p, "with_cds_match"),

_count_stage(z_p, "with_zspread"),

_count_stage(processed_p, "final_used"),

]

)

funnel["pct_of_prev_rows"] = (funnel["n_rows"] / funnel["n_rows"].shift(1) * 100).round(2)

funnel.loc[0, "pct_of_prev_rows"] = 100.0

funnel["pct_of_raw_rows"] = (funnel["n_rows"] / funnel["n_rows"].iloc[0] * 100).round(2)

print(f"Coverage funnel [{p_name}] - {p_label}")

display(funnel)

fig, ax = plt.subplots(figsize=(9, 4))

ax.bar(funnel["stage"], funnel["n_rows"], color="slateblue", alpha=0.85)

ax.set_title(f"Coverage Funnel by Stage [{p_name}]")

ax.set_ylabel("Number of rows")

ax.set_xlabel("Pipeline stage")

ax.grid(axis="y", alpha=0.3)

plt.xticks(rotation=20, ha="right")

plt.tight_layout()

plt.show()

Coverage funnel [replication_2010_2020] - Replication (2010-01-01 to 2020-02-29)

| stage | n_rows | n_unique_ids | pct_of_prev_rows | pct_of_raw_rows | |

|---|---|---|---|---|---|

| 0 | raw_bond_rows | 1013297 | 49042 | 100.00 | 100.00 |

| 1 | with_redcode | 110594 | 2298 | 10.91 | 10.91 |

| 2 | with_cds_match | 86270 | 1925 | 78.01 | 8.51 |

| 3 | with_zspread | 86149 | 1924 | 99.86 | 8.50 |

| 4 | final_used | 86149 | 1924 | 100.00 | 8.50 |

Coverage funnel [full_period_2010_2024] - Full Period (2010-01-01 to 2024-12-31)

| stage | n_rows | n_unique_ids | pct_of_prev_rows | pct_of_raw_rows | |

|---|---|---|---|---|---|

| 0 | raw_bond_rows | 2045502 | 115097 | 100.00 | 100.00 |

| 1 | with_redcode | 153943 | 2690 | 7.53 | 7.53 |

| 2 | with_cds_match | 118908 | 2244 | 77.24 | 5.81 |

| 3 | with_zspread | 118750 | 2243 | 99.87 | 5.81 |

| 4 | final_used | 118750 | 2243 | 100.00 | 5.81 |

10.2 Bond Counts (Monthly): Our Replication vs Authors#

fig, axes = plt.subplots(2, 1, figsize=(13, 9), sharex=True)

for ax, rating in zip(axes, ["Investment Grade", "High Yield"]):

s_our = our_rep[our_rep["c_rating"] == rating].sort_values("date")

s_auth = authors_monthly[authors_monthly["c_rating"] == rating].sort_values("date")

ax.plot(

s_our["date"],

s_our["n_bonds"],

label="Our replication",

linewidth=1.2,

color="steelblue",

)

ax.plot(

s_auth["date"],

s_auth["n_bonds"],

label="Authors",

linewidth=1.2,

color="darkorange",

)

ax.set_title(f"{rating}: Number of Bonds")

ax.set_ylabel("Bond count")

ax.grid(alpha=0.3)

ax.legend(loc="best")

axes[-1].set_xlabel("Date")

plt.tight_layout()

plt.show()